Europe’s judicial property auction market is often misunderstood.

It is tempting to describe it as a continent-wide stream of distressed bargains. That makes for a good headline, but it misses the reality. In 2026, Europe’s auction market is not being driven by a broad housing collapse. It is being shaped by something more complex: high property values, localized distress, uneven liquidity, fragmented public data, and legal processes that vary sharply from one country to the next.

That complexity is precisely what makes the market interesting.

For real estate investors, banks, servicers, and asset managers, judicial auctions remain one of the few parts of the European property market where information asymmetry still matters. The opportunity is not simply that assets may trade below market value. It is that the process itself is difficult to interpret, compare, and monitor at scale.

Europe’s housing market remains strong, but uneven

At the macro level, Europe’s housing market has proven far more resilient than many expected.

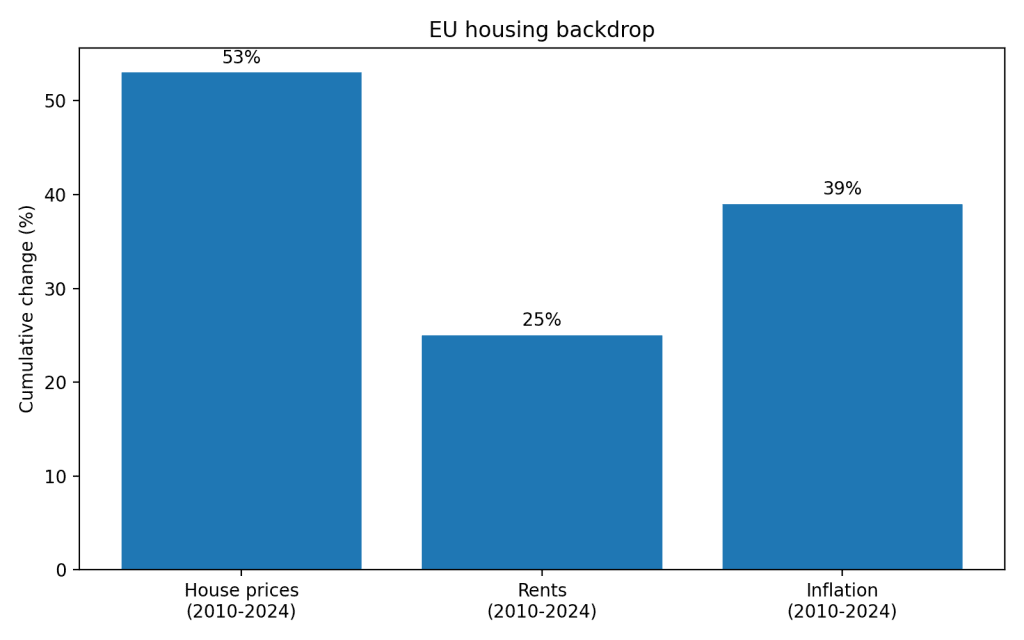

Between 2010 and 2024, house prices across the EU rose by 53%, while rents increased by 25%. In Q3 2025, EU house prices were still growing year on year. That is not the backdrop of a market in free fall. It is the backdrop of a market where housing remains structurally expensive, affordability is under pressure, and collateral values have held up better than feared.

This matters because judicial auctions do not exist in isolation. They sit downstream from affordability pressure, refinancing conditions, borrower distress, and national enforcement systems. When those forces move in different directions, the result is not one European auction market, but many local ones.

Distress exists, but it is not broad-based

The banking picture tells a similar story.

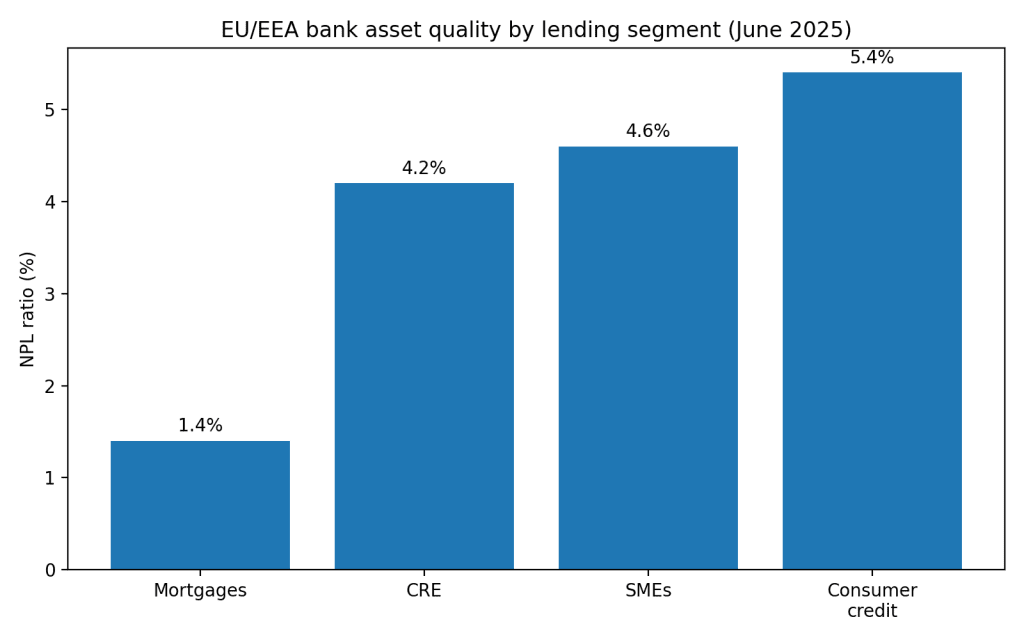

Across the EU and EEA, mortgage books remain relatively healthy. Non-performing loan ratios for residential mortgages are low by historical standards, while higher stress is more visible in areas such as commercial real estate, SMEs, and consumer lending.

That suggests a crucial distinction: Europe is not currently in a generalized mortgage-distress cycle. Instead, auction activity is being supported by more concentrated pockets of pressure — individual borrower distress, refinancing issues, legacy enforcement cases, local legal bottlenecks, and asset-specific complexity.

For investors, that changes the thesis completely.

Judicial auctions in 2026 are less a “distress flood” market and more a special situations market.

The real opportunity is not just lower prices

A common misconception is that judicial auctions are attractive simply because they are cheaper.

Price matters, of course. But in practice, the bigger edge often comes from process asymmetry.

Europe’s auction systems differ by country in ways that directly affect pricing:

- who runs the auction,

- how the asset is valued,

- how widely it is advertised,

- how much deposit is required,

- what minimum bid rules apply,

- how long the process takes,

- and how title transfer works afterward.

That means there is no single “auction discount” across Europe.

In some markets, the opening bid starts at or near market value. In others, the legal framework allows progressively lower thresholds in later rounds. In still others, the pricing floor can be far below appraised value.

So when people speak casually about “buying 40% below market,” they are usually oversimplifying. Judicial-auction discounts are not universal. They are procedural, country-specific, and highly dependent on competition, round structure, and asset quality.

Discount ranges vary sharply by market

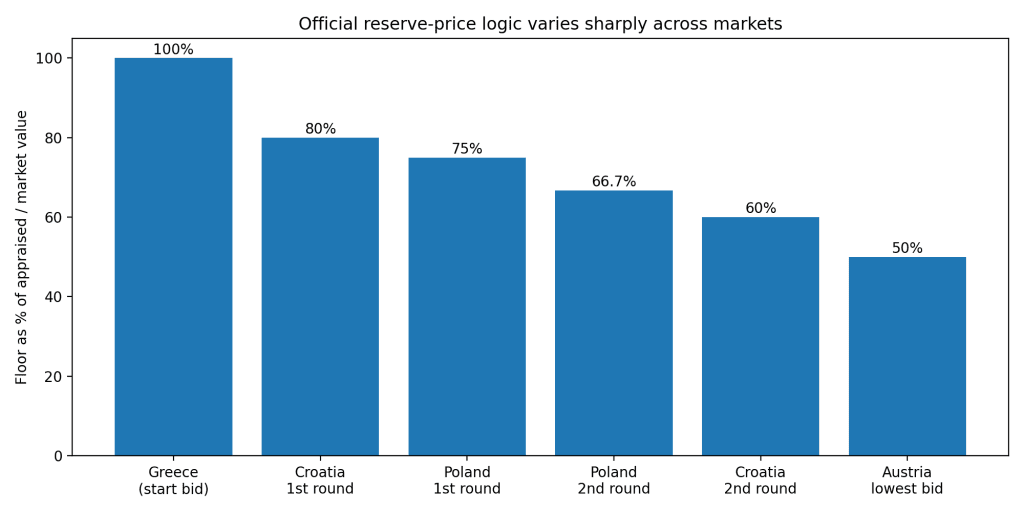

One of the clearest examples of this fragmentation is reserve-price logic.

In Greece, the starting bid for immovable property is tied to market value. In Croatia, the first online auction cannot sell below 80% of appraised value, while the second round can go down to 60%. In Poland, first-round pricing is typically 75% of appraised value and around two-thirds in the second round. Austria’s framework allows a much lower floor in some cases.

These rules do not determine the final transaction price by themselves, but they do define the boundaries within which price discovery happens.

For investors, this creates an important analytical distinction:

- headline discounts are market narratives,

- reserve floors are legal facts,

- realized pricing depends on bidder participation, documentation quality, and execution risk.

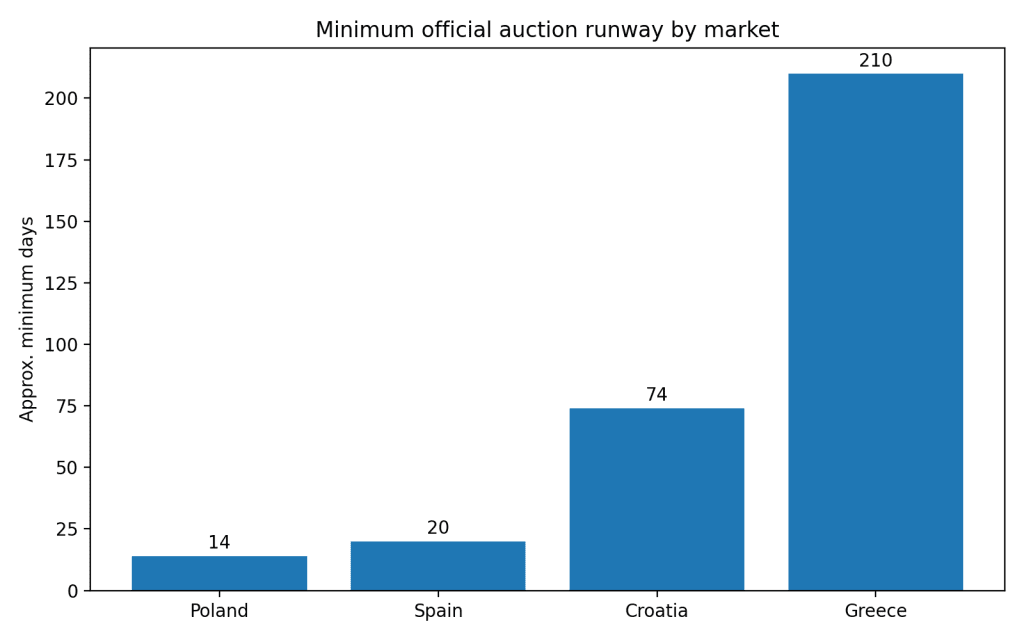

Time to sell depends on which clock you use

Another area where the market is often misunderstood is speed.

At first glance, judicial auctions can look efficient. Some bidding windows are short, digital, and transparent. But the real timeline is much longer than the live auction itself.

Spain’s judicial e-auctions typically run for 20 calendar days. Poland requires notice publication at least two weeks before the auction. Croatia requires at least 60 days between publication and the start of bidding, with bids then collected over 10 working days. Greece is slower still, with auction dates tied to a much longer procedural schedule following seizure.

That means “time to sell” in auctions is not the same as “days on market” in conventional brokerage.

A better way to think about it is procedural runway:

- how long before the auction goes live,

- when deposits have to be posted,

- how much time a buyer has to review documents,

- and how long ownership transfer takes after a successful bid.

In judicial auctions, time is part of the return profile.

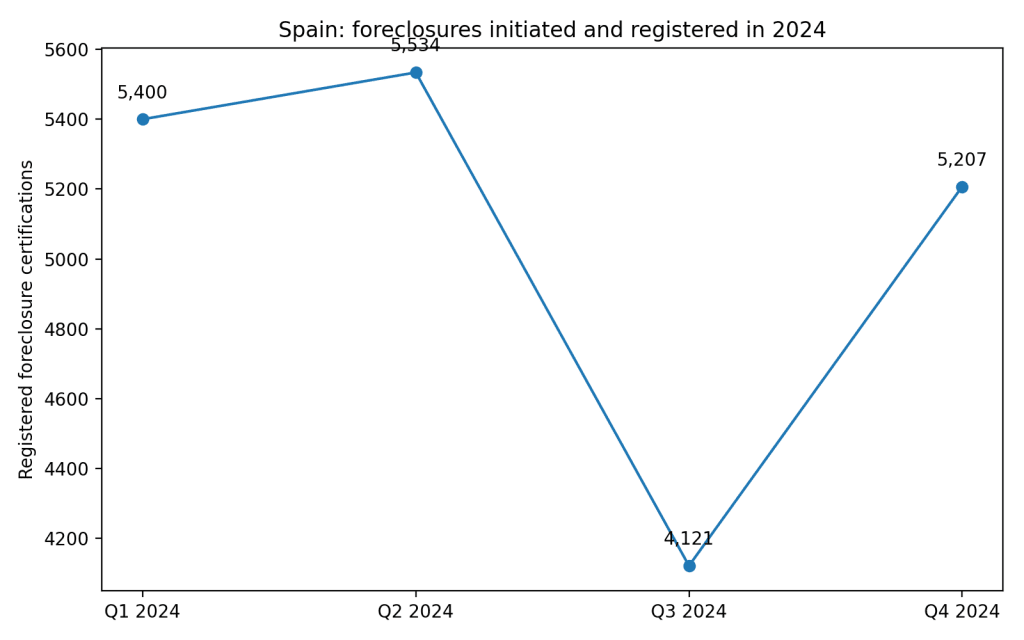

Spain offers one of the clearest live signals

Spain remains one of the most transparent large European markets for public-auction monitoring, thanks to its official digital infrastructure and national statistics.

The market shows active foreclosure flow, but not disorder. Foreclosure activity remains present, yet the data does not point to a market spiraling into systemic distress. Instead, it reflects a functioning enforcement ecosystem in a market where digitization has improved visibility without removing complexity.

That makes Spain a useful benchmark. It shows what happens when auction infrastructure becomes more transparent: buyers gain better visibility into volume and process, but the work of interpretation does not disappear.

Why auctions still matter in a recovering market

PwC and McKinsey both point to a European property market that is stabilizing and becoming more selective, not one that is experiencing a broad-based rebound across all segments.

That is exactly where auctions remain relevant.

They matter when:

- assets fall outside the easiest financing categories,

- title, occupancy, or legal issues make conventional buyers hesitate,

- documentation is fragmented,

- the process deters underprepared capital,

- or enforcement systems surface assets that are not efficiently distributed through ordinary brokerage channels.

In other words, auctions are still important not because the whole market is broken, but because parts of it remain inefficient.

And inefficiency is where specialist buyers still earn their edge.

The strategic takeaway for investors

In 2026, Europe’s judicial property auction market is best understood as an inefficiency market.

The inefficiency is legal.

The inefficiency is operational.

The inefficiency is informational.

Only sometimes is it purely about price.

That means serious investors should not focus only on the lowest possible bid. They should focus on:

- document interpretation,

- reserve-price tracking,

- procedural timing,

- title and encumbrance review,

- occupancy risk,

- and cross-market comparability.

The strongest buyers in this market are rarely the most aggressive.

They are usually the least confused.

Final word

Europe’s judicial auctions are not disappearing. Nor are they turning into a uniform, continent-wide bargain channel.

They are becoming more digital, but they remain fragmented. They are shaped by resilient property values, relatively contained mortgage distress, country-specific enforcement systems, and a level of procedural complexity that still keeps many buyers at a distance.

That is why this market continues to matter.

Not because it is easy.

Because it is still inefficient.

And in real estate, inefficiency is often where the most interesting opportunities begin.

CTA

Looking to track judicial property auctions across fragmented European markets more efficiently?

Book a demo of Bidsale® and see how VendueTech turns scattered public-auction data into structured real-estate intelligence for investors, banks, and asset managers.